Decomposing a $2.45B headline: Bayer / Perfuse through BioValue

On May 6, 2026, Bayer announced an acquisition of Perfuse Therapeutics for up to $2.45B: $300M upfront, $2.15B in development, regulatory, and commercial milestones.1 The asset is PER-001, a Phase II endothelin receptor antagonist delivered as a sustained-release intravitreal implant, in development for both diabetic retinopathy and glaucoma.

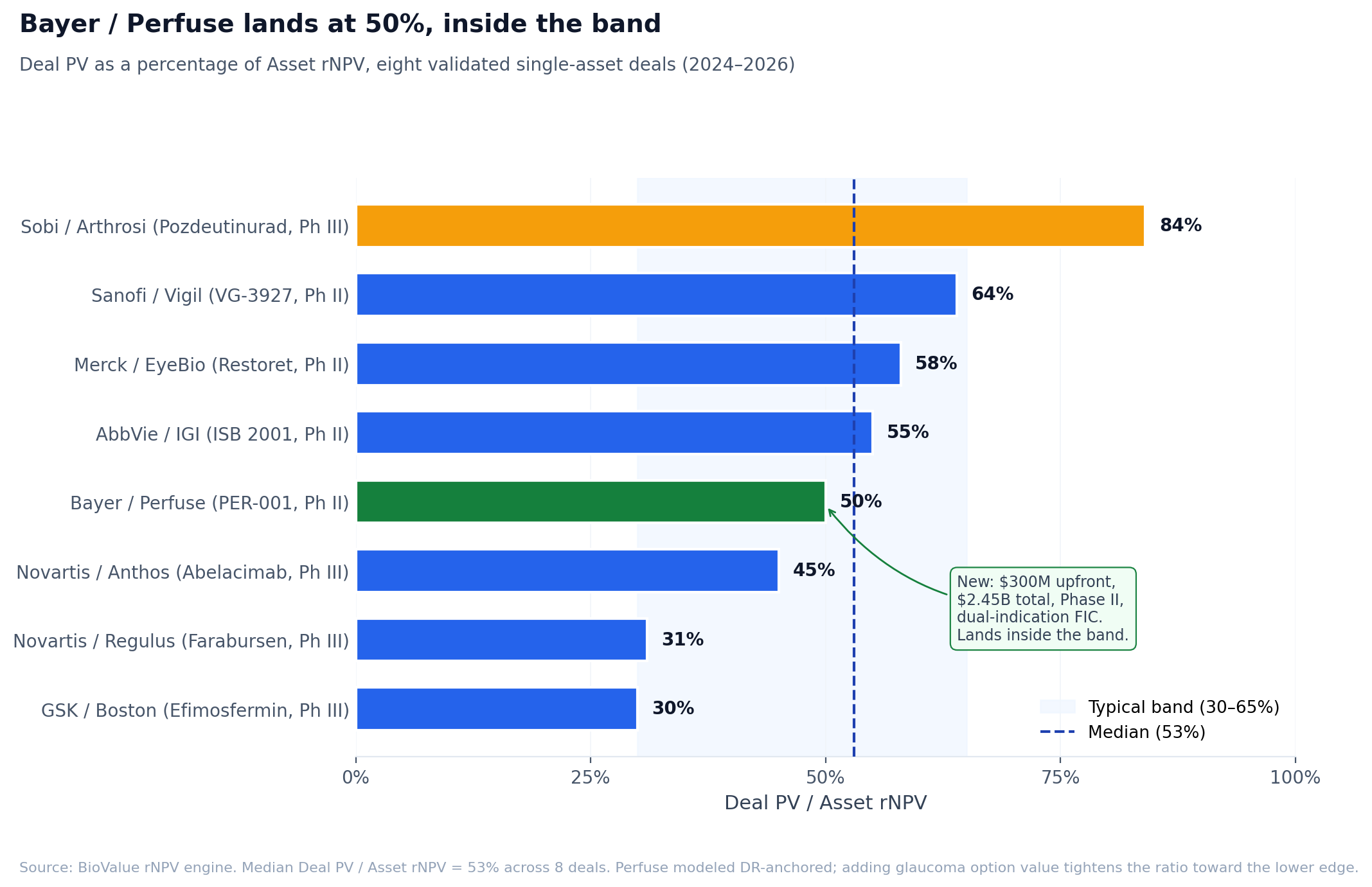

The headline reads aggressive: $2.45B for a Phase II asset. Run it through BioValue, and the math reads fair value.

What we know about the asset

PER-001 is a small molecule endothelin receptor antagonist formulated as a bio-erodible intravitreal implant.2 Sustained release, single-use 25-gauge applicator. Phase II for diabetic retinopathy (DR) and glaucoma. Perfuse positions PER-001 as a potential first disease-modifying treatment for both, contrasting with current anti-VEGFs targeting DME and IOP-lowering drops in glaucoma.

For modeling, anchor to DR. It is the larger high-value market and aligns with Bayer’s existing retina franchise around Eylea.

Stage: Phase II

TA: Ophthalmology

Modality: Small molecule (sustained-release implant)

Mechanism: Endothelin receptor antagonist

WACC: 8.0% (Bayer)

FIC flag on

Phase II to approval PoS in ophthalmology, FIC-stacked: roughly 35 to 40 percent3

Glaucoma upside is treated as option value, not modeled in the single-indication anchor.

Three-value framework

Standalone Asset rNPV (Bayer 8.0% WACC, FIC, DR-anchored, ~18% peak share):

Roughly $1.5 to $2.0B central case, $1.8B point estimate.

Commercial-adjusted lower bound (14% WACC, peak × 0.60, commercial PoS × 0.85):

Roughly $450 to $600M. The BD-realistic floor.

Deal PV (acquisition, no royalty):

Upfront: $300M, fully present-valued

Risk-adjusted dev milestones PV: ~$200M

Risk-adjusted regulatory milestones PV: ~$150M

Risk-adjusted commercial milestones PV: ~$280M

Total Deal PV: roughly $800M to $1.0B, $900M point estimate.

Where this lands

Deal PV / Asset rNPV ≈ 45 to 55 percent.

That sits inside the 30 to 65 percent empirical band.4

The $2.45B headline tells you very little. The components tell you almost everything:

$300M upfront is roughly 12 percent of the headline. That is within the typical 5 to 20 percent range for Phase II acquisitions.

$2.15B in milestones is aspirational. Risk-adjusted to today, those milestones contribute only $600 to $700M of present value.

No royalty, because this is an acquisition. Bayer captures full economics post-close, so the licensing-deal royalty layer disappears.

Risk-adjusted Deal PV of $0.9B against a single-indication Asset rNPV of $1.8B is a fair-value transaction by every comp in the BioValue validation set. The deal looks aggressive in press release dollars because the milestones are nominal, not present-valued.

The glaucoma option

Single-indication anchor understates what Bayer is buying. PER-001 has a Phase II program in glaucoma, and the disease-modification claim positions it for a premium segment of a much larger patient population (around 3 million US glaucoma patients versus around 1 million treated DR patients).

If glaucoma is added as a second commercial indication at roughly 50 percent of DR’s peak revenue contribution, Asset rNPV broadens from $1.8B central to roughly $2.7B. Deal PV / Asset rNPV drops to 30 to 40 percent, still inside the band, just at the lower edge.

The dual-indication framing doesn’t change the conclusion. The deal is inside the band either way.

The structural read

Three things show up in this deal that don’t show up in the headline:

Strategic context. Bayer’s Eylea franchise is exposed to biosimilar erosion. PER-001 is a pipeline rebuild bet for the retina business. The asset has a franchise role, not just a standalone NPV.

Dual indication. Single-asset rNPV anchored to DR ignores glaucoma option value. Adding glaucoma tightens Deal PV / Asset rNPV from mid-band toward lower-band.

No royalty. Acquisition structure means Bayer captures full economics post-launch. For a licensing deal of similar economics, the royalty stream would shift Deal PV up by 20 to 30 percent.

The takeaway

Headlines optimize for press release optics. Decomposing a deal into upfront + risk-adjusted milestones + (when applicable) royalty PV is what tells you whether a buyer overpaid. By that decomposition, Bayer paid fair value for a Phase II FIC ophthalmology asset with a strategic franchise role and dual-indication option value.

The 30 to 65 percent band keeps holding. Aggressive-looking headlines aren’t the same as premium pricing. They’re the headline number multiplied by the milestone risk discount.

The deal is now a Perfuse preset in BioValue.5 Toggle the share assumption, layer in glaucoma, watch the band move.

[1] Bayer press release, May 6 2026; Fierce Biotech and Pharmaphorum coverage.

[2] Perfuse Therapeutics company communications.

[3] MIT Project ALPHA, phase-transition probability database (ophthalmology small molecule, Phase II to approval).

[4] BioValue Substack, “Single-asset drug deals…”.

[5] nealvybe.github.io/biovalue, Perfuse / PER-001 preset.

| A guest post by

|